General Ledger Posting Tutorial

View the chapter video before beginning this lesson.

As we learned in the last lesson, each business transaction is recorded in a specialized journal.

- The journal does not sort the entries into accounts.

- The journal does not show in one place, for example, utilities expense.

- A journal does not supply account balances for preparing up-date financial records.

- In order to see how transactions have changed account balances, posting from the different journals to the accounts is necessary.

- Posting is a simple sorting process that transfers amounts from the journals to the appropriate accounts in the ledger.

- If you look at the Chart of Accounts below, you will see that the ledger is arranged in the same order as they appear in financial reports.

- The assets, liabilities and stockholders' equity accounts are on the balance sheet.

- The revenue and expense accounts are on the income statment.

- The ledger is arranged in the same manner.

- We need to look first at Bromley's Formal Wear General Ledger.

- Click on the link above to view the general ledger.

- Account names and numbers are filled in

- As you can see they match the chart of accounts.

- They are arranged by type of account: assets, liabilities, stockholders equity, sales, cost of merchandise sole and expenses.

An Excel spreadsheet called Journal Summary has been prepared for you. You may wish to print it out and use it while you are posting. The information is the same that is contained in the all of the journals.

Bromley's Formal Wear |

Chart of Accounts |

| Account Number | Account Name |

ASSETS (1) |

| 111 | Cash |

| 112 | Accounts Receivable |

| 113 | Furniture and Fixtures |

| 114 | Accumulated Depreciation Furniture |

| 115 | Office Supplies |

| 116 | Other Assets |

| 117 | Office Equipment |

| 118 | Accumulated Depreciation Office Equipment |

| 119 | Prepaid Insurance |

| 120 | Inventory |

LIABILITIES (2) |

| 211 | Notes Payable |

| 212 | Accounts Payable |

| 213 | Workers' Comp Payable |

| 214 | Federal Income Tax Payable |

| 215 | FICA Tax Payable |

| 216 | Medicare Payable |

| 217 | FUTA Payable |

| 218 | SUTA Payable |

| 219 | Sales Tax Payable |

| 220 | SDI Payable |

| 221 | State Income Tax Payable |

| 222 | State Training Tax Payable |

STOCKHOLDERS' EQUITY (3) |

| 311 | Common Stock |

| 312 | Retained Earnings |

REVENUE (4) |

| 411 | Sales |

| 412 | Sales Returns |

| 413 | Other Income |

COST OF MERCHANDISE SOLD (5) |

| 511 | Purchases |

| 512 | Purchase Returns |

EXPENSES (6) |

| 611 | Salary Expense |

| 612 | Rent Expense |

| 613 | Repairs Expense |

| 614 | Advertising Expense |

| 615 | Supplies Expense |

| 616 | Depreciation Expense |

| 617 | Insurance Expense |

| 618 | Miscellaneous Expense |

| 619 | Payroll Taxes Expense |

| 620 | Legal and Accounting expense |

| 621 | Utilities Expense |

| 622 | Alterations Expense |

| 623 | Interest Expense |

| 624 | Delivery Expense |

POSTING FROM THE GENERAL JOURNAL

We are going to post the entries from the general journal to the general ledger. Open the General ledger. The link is in the Projects box.

- The first one is to record the loan.

- The amount of the loan was for $15,800.00.

- The amount was determined by the items that we needed to start up our business: Furniture & Fixtures, Office Equipment, Supplies, and Merchandise Inventory.

- As you can see two accounts, Cash and Notes Payable are involved in this tranasaction.

- Let's post the Cash account first.

- In cell A8, type in the date of the posting , 11-1

- In cell C8, type GJ1. This is the posting reference and states that this number came from the General Journal, Page 1

- In Cell D8, type in 150,800. This where the first debit posting to this account goes.

- The debit total column shows 150,800

- The balance in the account shows 150,800 debit balance.

- Find the Notes Payable account. It is a liability account so, scroll down until you see it.

- In cell A103 enter the date, 11-1

- In cell C103, type GJ1 as the posting reference

- In cell E103, type in the amount of the posting, 150,800

- The total of the credits posting to the account shows at the bottom

- The account balance is a credit balance of 150,800.

- Post the second entry from the General Journal, the one relating to common stock and cash.

- Follow the same procedure as listed above.

- Cash Posting

- Cell A9 for the Date, 11-1

- Cell C9 for posting reference, GJ1

- Cell D9 For the debit amount of, 85,000

- Common Stock Posting

- Cell A217 for the Date, 11-1

- Cell C217 for the posting reference, GJ1

- Cell E217 for the credit amount of 85,000

- Post the next two entries for salary expense and payroll taxes in the same manner as instructed above.

- How do you know if you posted correctly?

- Read the short tutorial on trial balance, then scroll down to the bottom of the worksheet to see if you are in balance after posting these four entries.

- Save your file and turn in a printout toyour instructor.

POSTING FROM THE CASH RECEIPTS JOURNAL

Look at the bottom row of the cash receipts journal to find the amounts that need to be posted. These are the numbers we want to post. They are summarized for your convenience.

The cell locations on the ledger spreadsheet, posting references, date and amounts are summarized in the table below.

| Date | Post Ref | Amount |

| Sales |

Cell A236 - 11/30 | Cell C236 - CR1 | Cell E236 - $316,270.01 |

| Sales Tax Payable |

Cell A179 - 11/30 | Cell C179 - CR1 | Cell E179 - $10,899.59 - $316,270.01 |

| Cash |

Cell A11 - 11/30 | Cell C11 - CR1 | Cell E11 - $327,169.60 |

Scroll down to the trial balance and see that you are still in balance after posting the cash receipts journal. Save your file and turn in a printout to your instructor.

POSTING FROM THE CASH PAYMENTS JOURNAL

If you will remember in the cash payments journal, we used account numbers as codes to record the debit part of the transaction. These code numbers are the account numbers where we want to post these amounts. For example, if we want to post the total amount of salaries we would post it to account 611.

To begin the posting process, follow these steps.

- Click on the link for the Cash Payments Journal

- Scroll down to row 30. These are the numbers to be posted to the general ledger

- The table below shows which accounts are debited and credited, the amount to be posted and the cell number in the general ledger where the amount should be entered.

- You will also need to supply the date of the transaction and the post ref showing that the posting came from the cash payments journal (cp1)

- You notice that all accounts in the cash payments journal are debited with the exception of Cash which is credited the total amount of all the debited accounts.

| Account Debited | Account credited | Amount | Post to Cell |

| Cash | 284,406.45 | E12 |

Furniture & Fixtures | | 47,000.00 | D27 |

Office Equipment | | 3,800.00 | D65 |

Mdse. Inventory | | 100,000.00 | J84 |

Notes Payable | | 655.54 | D104 |

Fed Inc Tax Payable | | 20,497.70 | J123 |

FICA | | 14,776.66 | D143 |

Medicare | | 3,455.84 | J143 |

FUTA | | 953.33 | D161 |

State Income Tax | | 6,267.50 | D199 |

SUTA | | 4,051.67 | J161 |

Sales Tax | | 10,899.59 | D180 |

SDI | | 595.83 | J180 |

State Training | | 119.17 | J199 |

Purchases | | 60,858.42 | J255 |

Advertising Expense | | 1,000.00 | D132 |

Delivery Expense | | 25.00 | D407 |

Insurance Expense | | 812.50 | J331 |

Interest Expense | | 1,508.00 | J388 |

Miscellaneous Expense | | 200.00 | D350 |

Repairs Expense | | 350.00 | J293 |

Supplies Expense | | 135.00 | J312 |

Alterations Expense | | 459.25 | D388 |

Rent Expense | | 3,750.00 | D293 |

Utilities Expense | | 2,187.50 | J369 |

Scroll down to the trial balance section and verify that you are still in balance before continuing. When you are in balance, save your file. Turn in a printout to your instructor.

POSTING FROM THE SALES JOURNAL TO GENERAL LEDGER

Look at the bottom row of the sales journal to find the amounts that need to be posted.

- Total Sales - Cell E11

- Sales Tax Payable - Cell F11

- Accounts Receivable - Cell G11

The cell locations on the ledger spreadsheet are summarized below.

| Account Debited | Account credited | Amount | Post to Cell |

Accounts Receivable | | 18,686.97 | J8 |

| Sales Tax | 1,384.22 | E181 |

| Sales | 17,302.75 | E237 |

Scroll down to the trial balance section and verify that you are still in balance before continuing. Total debit and credit check amounts are 570,592.57 When you are in balance, save your file and turn in a printout to your instructor.

POSTING TO THE ACCOUNTS RECEIVABLE LEDGER FROM THE SALES JOURNAL

In addition to our posting to the general ledger, we need to post individual charge sales and payments to our charge sales customers' accounts. Remeber that accounts receivable is an asset account. The money listed here represents money that you need to collect from customers that bought merchandise from you on account. The accounts receivable ledger is where you keep track of all of these charge sales.

The debit posting to the accounts receivable ledger comes from the sales journal.

Click on the sales journal link in the projects box to see the sales journal again.

- The people's name listed here are the accounts that need to have amounts posted to the accounts receivable ledger.

- Scroll over in the sales journal until you see the column headed "A/R Debit" .The amounts listed in this column will be posted as debits to their individual accounts.

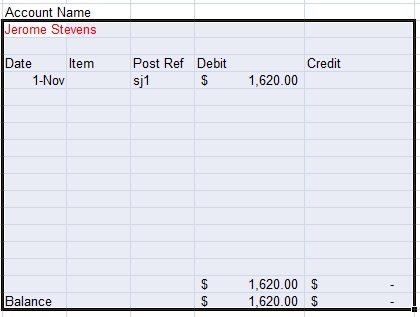

- The first customer that charged some merchandise is Jerome Stevens. He owes us $1,620.

- Proceed as follows to post this amount to Jermone Stevens' account.

- Click on the Accounts Receivable Ledger link.

- You should now see the accounts receivable ledger.

- Find his account

- On the first line under the heading "Date Item Post Ref Debit Credit", key in

the date 11-1

- The post reference SJ1

- The debit amount 1,620.00

- Look at the picture below to see how it looks when done.

- Continue to post the individual AR Debit amounts to all of the customers listed in the sales journal.

- Kenny Sanches

- Maryanne Thompson

- Rob Jones

- Charles Jamison

- Janet Coy

Posting to Accounts Receivable Ledger Fron the Cash Receipts Journal

Even though no charge sales customers have paid yet, It is important to review the procedures for recording a payment on account.

- The cash receipts journal shows cash received from cash sales and received on account amounts from charge sales customers.

- We are interested here in the payments made to Bromley's Formal Wear from our charge sales customers.

- Below is a sample cash receipts journal for illustration purposes.

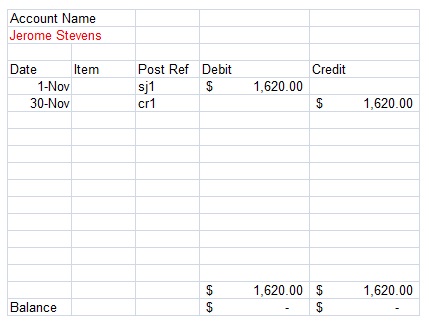

On November 30, Jerome Stevens sent us a check for $1,600.00. We need to post this payment to his accounts receivable ledger card to show that he has paid us. The example below show how this entry should look.

| Cash Receipts Journal |

Dt | Doc# | Acc Title | PR | Gen Credit | Sales Credit | Sales Tax Pay | AR Credit | Cash Debit |

11/14 | R1101 | Jerome Stevens | √ | |

| | $1,620 | $1,620 |

- The date is listed.

- The Doc # is next. It is a receipt number.

- The customer's name is next.

- The accounts receivable credit is the next column

- The Cash Debit column is next.

- The number we want to post is the Accounts Receivable Credit

- The posting to the accounts receivable account for Jerome Stevens shows:

- Date - November 30

- Item

- Post Reference shows that this entry came from the Cash Receipts journal.

- The credit to Accounts Receivable - $1,620.00

- The debit to Cash - $1,620.00

- Each money column has a total near the bottom of the form

- The balance in this account, as you can see is now zero after posting the accounts receivable credit on November 30.

Now it is time to verify that the total of the schedule of Accounts Receivable, from the accounts receivable ledger matches the accounts receivable total in the general ledger. The number should be the same.

Save the file and turn in a printout to your instructor.